AI Investment Has Entered Bubble Territory

When Billion-Dollar Bets Meet Uncertain Business Models

Last week, the stock market had a panic attack about AI. Oracle crashed 11% in a single day. Broadcom followed with its own 11% nosedive. Nvidia dropped 3%. AMD fell 4%. The S&P 500 shed over 1% on Friday alone.

If you have any money in the stock market, you probably have at least some exposure through index funds. Nvidia alone represents over 7% of the S&P 500. Add in all the other AI names like Palantir, Oracle, and Broadcom, and you’re talking about a massive chunk of the market suddenly looking shaky.

So what spooked everyone?

Two earnings reports that, in a more bullish market, should have been celebrated. Broadcom reported record revenue and strong AI chip demand. Oracle beat earnings. Both should have sent stocks soaring. Instead, investors ran for the exits.

The market’s message was clear: We’re not sure this AI boom is real anymore. And if the market’s right, your portfolio is about to get a lot more complicated.

The House of Cards Starts at the Top

At the top of this fragile pyramid sits OpenAI, the company behind ChatGPT. And unlike its competitors, OpenAI is burning money at a genuinely alarming rate. OpenAI’s revenue in the first half of 2025 reached $4.3 billion, already surpassing its full-year 2024 revenue. However, due to persistently high R&D expenditures, the company posted an operating loss of $7.8 billion. That’s not a typo. They made $4.3 billion and lost $7.8 billion in six months.

For context, OpenAI reported losses of $5 billion in 2024 on $3.7 billion in revenue, and projections suggest they could lose $14 billion by 2026, with total losses from 2023 to 2028 expected to reach $44 billion. But what makes this existential is that OpenAI doesn’t have a clear path to profitability, and its once-invisible lead is vanishing.

Sam Altman told employees in an internal memo on Monday that he was declaring a “code red” to dedicate resources toward bettering ChatGPT, given the pressure from rivals, particularly after Google’s Gemini 3 beat ChatGPT on benchmark tests and lured away users.

This isn’t just corporate drama. OpenAI has committed to spending commitments in the range of $1.4 trillion over the next decade while making nowhere near enough revenue to justify that. And if OpenAI can’t deliver on its promises? The entire house of cards falls.

The Infrastructure Players: Caught in the Cascade

Here’s where OpenAI’s problems become everyone else’s problems. The AI data center ecosystem comprises two types of players: the financially disciplined and the desperately overleveraged.

The “good” players—Microsoft, Google, Amazon—have strong balance sheets. They were building data centers long before the AI boom for their existing cloud businesses. Amazon Web Services (AWS), for instance, was initially built to meet Amazon’s e-commerce needs. These companies are financially disciplined. They build incrementally, adjusting to demand, ensuring what they build gets used at full capacity. They’re not gambling. They’re investing.

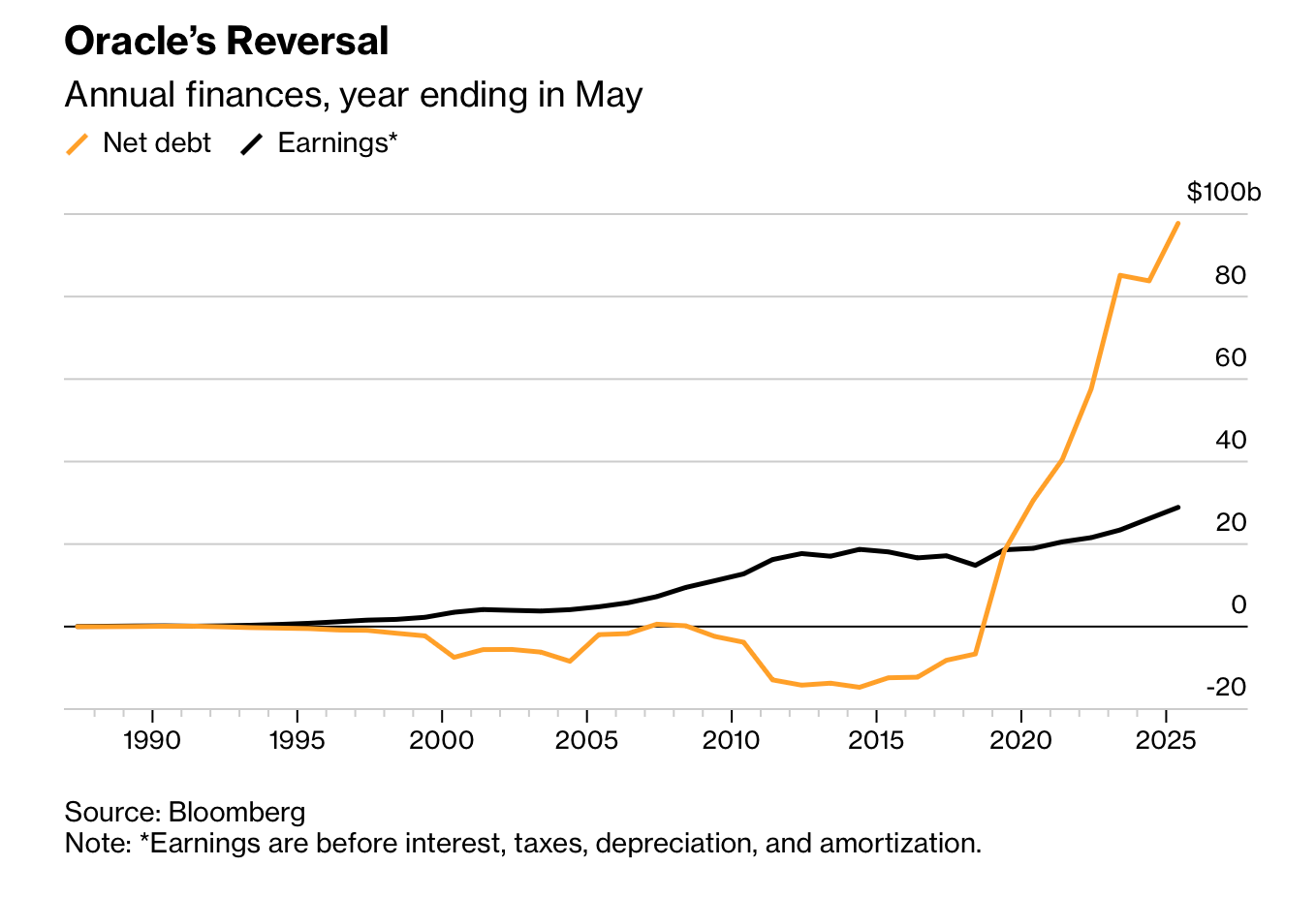

Then there are the “bad” players. Companies that want in on this AI gold rush but lack the luxury of taking it slow. Oracle is the poster child. Having missed the earlier cloud boom, they’re now taking on massive debt to catch up. Oracle disclosed a $15 billion increase in expected fiscal 2026 capital expenditures and flagged delays related to OpenAI-linked data centers, fueling skepticism about whether these investments will ever pay off. Bloomberg analysts pointed out the company needs to absorb $70 billion in free cash flow over the next decade just to pay off its current spending commitments.

The Chip Manufacturers: The Final Domino

OpenAI’s problems don’t stay with OpenAI. They cascade downstream to chip manufacturers like Nvidia and AMD. If OpenAI can’t fulfill its commitments to companies like Oracle, how does Oracle fulfill its promises to Nvidia to buy all those chips? Broadcom warned that a growing mix of lower-margin custom AI processors could squeeze profitability, raising the worry that some “AI winners” may be less lucrative than the market priced in.

That matters because these companies have become cornerstone investments for millions of people through index funds. Nvidia’s CEO Jensen Huang keeps saying demand outpaces supply. But what if that demand is driven by a few massive customers like OpenAI who can’t actually afford their commitments? That’s concentration risk at its most dangerous.

And it’s tying everyone together in increasingly precarious ways, what is referred to as circular deals. For instance, OpenAI committed to purchase Nvidia GPUs after Nvidia invested a reported $100 billion in the company. (Note: Nvidia noted in its recent earning that there is “no assurance” of agreement with OpenAI despite $100 billion pact). Everyone’s financially knotted together, and if one thread snaps, the whole thing unravels.

Reuters reported that AI data center and project financing deals surged to $125 billion so far this year (versus $15 billion in the same period of 2024), citing a UBS report, with more supply expected to matter for credit markets in 2026. Even the Bank of England warned that debt’s growing role in AI infrastructure could heighten financial stability risks if valuations correct.

While bubbles do destroy tremendous wealth, they also serve to fund the development transformative technologies. The fiber optic investments of the late ‘90s bankrupted companies but gave us the internet infrastructure we use today. While the current AI spending spree might bankrupt some companies and destroy billions in market value, it does also builds the foundation to a genuinely world-changing technology.

The question isn’t whether AI is real or valuable. It obviously is. The question is whether the current spending levels are sustainable, whether the companies burning billions have viable business models to pay for those investment in due time. And perhaps most importantly, whether your investments are diversified enough to withstand the risk and volatility.