Are We in an AI Bubble? A Bubble Gum Explainer

AI this, AI that. You can’t scroll through TikTok, open LinkedIn, or even order coffee without someone mentioning artificial intelligence. Your reaction to that sentence probably falls into one of two camps: either you’re hyped (AI is going to change everything!) or you’re exhausted (can we please talk about something else?).

But here’s where things get real: everyone agrees AI will transform our world—it already is. The actual question keeping people up at night isn’t whether AI matters, but whether we’re living in a bubble. And yeah, the type that can pop and wreck your financial future.

If you don’t remember 2008, ask your parents. When the housing bubble burst, it triggered a two-year recession. The S&P 500 plummeted 57% between October 2007 and March 2009. Real money evaporated. Home prices cratered by 20% or more in some areas. It took years for the market to recover, and some people never did.

So the question hanging over every AI investment, every tech stock, every startup pitch is this: Are we about to watch history repeat itself?

Understanding Bubbles (Yes, Like the Gum)

If you’ve ever blown a bubble with gum, congratulations—you already understand financial bubbles better than most people on Bloomberg or CNBC.

The mechanics are literally that simple. You blow air into the gum until it stretches into a balloon. Keep blowing, and eventually? Pop. The bubble collapses because it can’t hold any more air.

Financial bubbles work the same way, except instead of air, we’re pumping in money. During the 2008 housing crisis, money flooded into real estate—more and more capital chasing the same assets—until the market couldn’t sustain it anymore. Then it popped.

The Role of Leverage (AKA Debt)

Here’s where it gets spicy: leverage. That’s just a fancy word for borrowing money, and you probably use it more than you think. Every time you swipe your credit card, you’re technically in debt (hopefully just until next month). Student loans, car loans, mortgages—all debt, just paid back over different timelines.

Debt isn’t inherently bad. Private equity firms use it to boost returns. You use it to finance your education. But in a bubble, debt becomes the problem. When everyone’s borrowing massive amounts to buy an asset, it drives prices higher and higher. The valuation—what people think something is worth—stretches further and further from the fundamentals—what it should be worth.

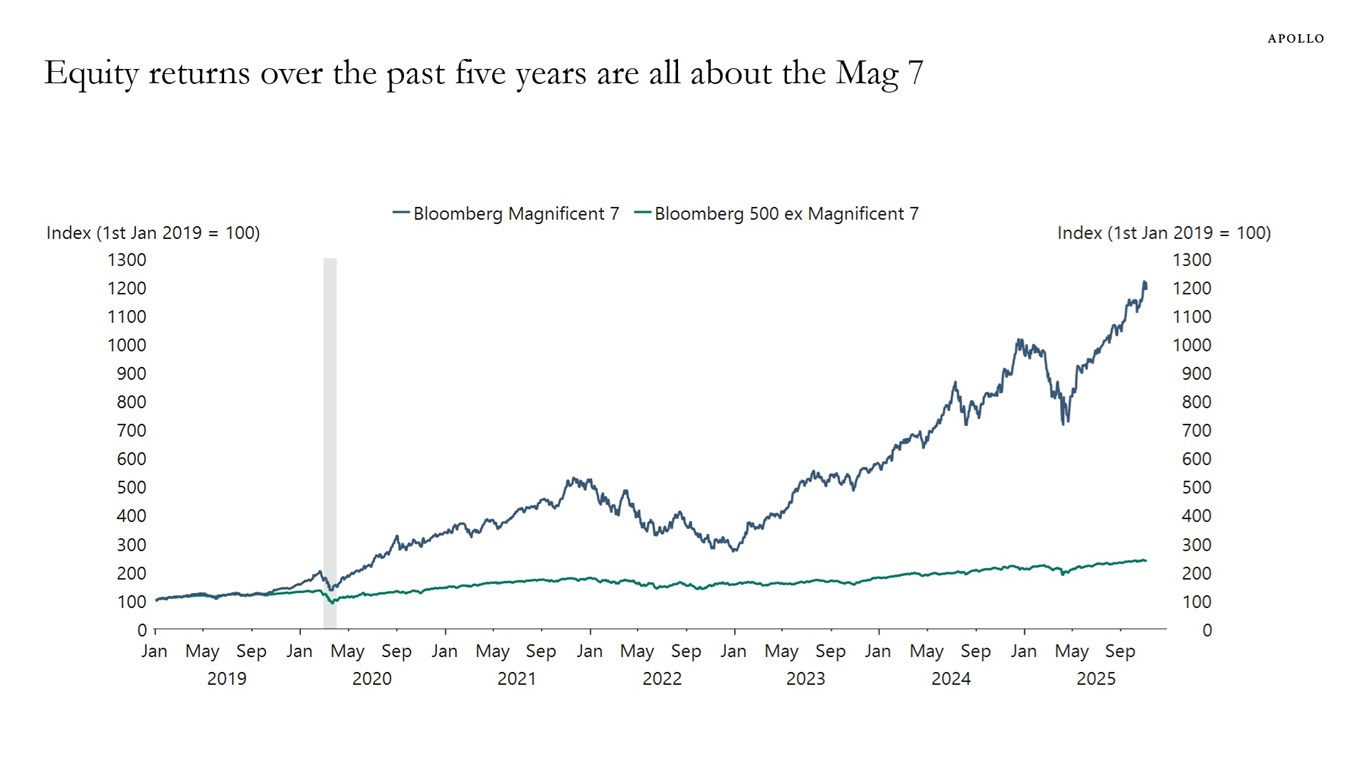

And that gap? That’s where the danger lives. Right now, Nvidia just became the first company ever to hit a $5 trillion market valuation, and just five years ago, its market cap sat around $100 billion—a fiftyfold increase driven almost entirely by AI demand. That’s the kind of explosive growth that makes people nervous.

The Psychology of Believing Your Own Hype

But how do you know what something should be worth? Plot twist: you don’t. Not exactly.

You don’t know precisely how much air you can blow into gum before it pops. You don’t know exactly when the housing market will crash. But an experienced bubble blower will tell you there are signs—the gum gets thin, it wobbles, you can almost feel it reaching its limit.

Markets work the same way. You can watch indicators: Are prices accelerating faster than historical averages? Is the increase fueled by debt? Most importantly, is everyone getting increasingly hyped, driven by pure exuberance?

Here’s where the numbers get interesting. Tech firms now make up 49% of the S&P 500’s market capitalization—eerily close to the 47% they hit at the peak of the dot-com bubble in 2000. But there’s a crucial difference: today’s “Magnificent 7” tech stocks trade at a price-to-earnings ratio of 38.3x, while the “Four Horsemen” of the dot-com era (Intel, Microsoft, Cisco, Dell) traded at an extremely pricey 82.7x.

Translation? Tech stocks are expensive, but not that expensive. At least not yet.

Because here’s the thing: for a bubble to grow, everyone has to believe the same story. Everyone has to think prices will keep rising, or at least believe they’re smart enough to get out before it bursts. That requires excitement, enthusiasm, conviction. But any experienced bubble blower knows that the more excited you get, the more likely you’ll lose control and—pop.

The current story goes like this: AI is going to revolutionize everything, and early investors will be rewarded beyond measure. And to back it up, tech giants Meta, Amazon, Alphabet, and Microsoft plan to spend over $380 billion combined on AI infrastructure in 2025, up from $230 billion in 2024. That’s 1.28% of US GDP—approaching levels seen during the Manhattan Project and the Apollo moon landing.

That’s not hype money. That’s “we’re betting the company on this” money.

What Makes Bubbles Pop?

Several things can burst a bubble. Sometimes it’s simply too much air—too much leverage, too much money, not enough fundamental value to support it. Prices drop because there’s literally no more capital to pump in.

Other times, it’s an external shock. Your friend poking your bubble gum. In markets, this could be a narrative shift (”wait, are homes actually overpriced?”), rising interest rates, an economic slowdown—what economists call exogenous shocks. Something from outside the system that disrupts the belief holding everything together.

Here’s what’s making investors nervous: AI companies are spending $400 billion per year on infrastructure, but OpenAI—the biggest AI company—has disclosed revenues of just $13 billion for 2025 and may have lost $12 billion in the third quarter alone. That’s a massive gap between spending and revenue. The investment has to pay off eventually, or the whole thing unravels.

But there are also reassuring signs. Nvidia just reported that demand for its AI chips is “off the charts,” with $500 billion in orders already on the books for 2025 and 2026 combined. Real companies are placing real orders, not just speculating on future potential.

And what happens after a bubble pops? Usually, another one forms. People dust themselves off, convince themselves “this time will be different,” and find a new asset to get excited about. We’ve seen it with railways in the 1840s, the dot-com boom in the late ‘90s, housing in 2008. Now, possibly, AI. Other countries experience them too—look at China’s real estate bubble that collapsed a few years ago.

The tricky part? Bubbles are hard to spot while you’re inside them. It’s psychologically difficult to think contrary to what everyone around you believes. Try telling someone in 2006 that home prices would crash and they’d look at you like you’d grown a second head (try that today, and you’ll get the same reaction). Right now, the S&P 500’s Shiller P/E ratio sits at 39.8—just below the 44.2 peak that preceded the 2000 crash, making it the third-highest valuation in 154 years of market history.

That should make anyone pause.

Conclusion: So... Are We in an AI Bubble?

Here’s the honest answer: nobody knows for sure. Not your econ professor, not the talking heads on financial news, not the VCs dumping billions into AI startups, and certainly not me.

The people who successfully called previous bubbles—legends like Michael Burry (watch The Big Short if you haven’t) or economist Robert Shiller (read Irrational Exuberance)—they didn’t have a crystal ball. They looked at indicators, trusted their analysis despite everyone thinking they were crazy, and got lucky with their timing. Even they couldn’t tell you with certainty when things would collapse, just that the fundamentals didn’t add up.

The data we have paints a complicated picture. Yes, tech valuations are high and AI spending is astronomical. But unlike the dot-com bubble, today’s tech companies are actually profitable, with profit margins at 26%—more than double the levels seen in 2004. These aren’t companies burning cash with no business model. They’re generating real revenue and real profits.

Still, U.S. tech stocks now account for about 60% of all global stock market valuation, with technology stocks representing 45% of all U.S. stocks. That’s a lot of eggs in one basket. If AI doesn’t deliver on its promises, or if it takes longer than expected, the fallout could be significant.

So if you’re feeling uncertain, confused, or a little anxious about whether we’re in an AI bubble, join the club. That uncertainty is actually rational. Anyone claiming to know for certain is either lying or delusional.

The point isn’t to predict the future with perfect accuracy. It’s to understand the mechanics—to recognize the signs of excess, to question narratives when they seem too good to be true, to distinguish between genuine innovation and hype-fueled speculation.

Because now you know what a bubble actually is. And it really isn’t more complicated than bubble gum.

Next time someone at a party starts ranting about “the AI bubble,” or you see yet another breathless headline about whether tech stocks are overvalued, you don’t need to panic or pretend to understand complicated financial jargon. Just think about blowing a bubble. Feel the gum stretch. Notice when it starts getting thin and unstable. Pay attention to how much air you’re pumping in, and how excited you’re getting.

And remember: the bubble always feels solid and real—right up until the moment it pops.

P.S. For those of you with a more technical background, I recommend this piece by Neutral Foundry that break down why Michael Burry’s Big Short 2.0 might be wrong this time.