The House We’ll Never Own

Home ownership? That's up in the air

There is a particular kind of math that a lot of people in their twenties have started doing late at night, usually after stumbling across a real estate listing they had no real intention of pursuing. The average detached house in Toronto sits around $1.5 million CAD. In Vancouver, closer to $2 million. A reasonable salary, decent savings habits, taxes taken out — and still, the number on the screen feels less like a price and more like a verdict.

That feeling — that specific, quiet despair of watching homes being financially out of reach — explains why so many young people are gambling on zero-day options, piling into meme coins, splurging on $400 concert tickets and $6,000 trips to Japan, and generally behaving in ways that look, from the outside, like financial nihilism.

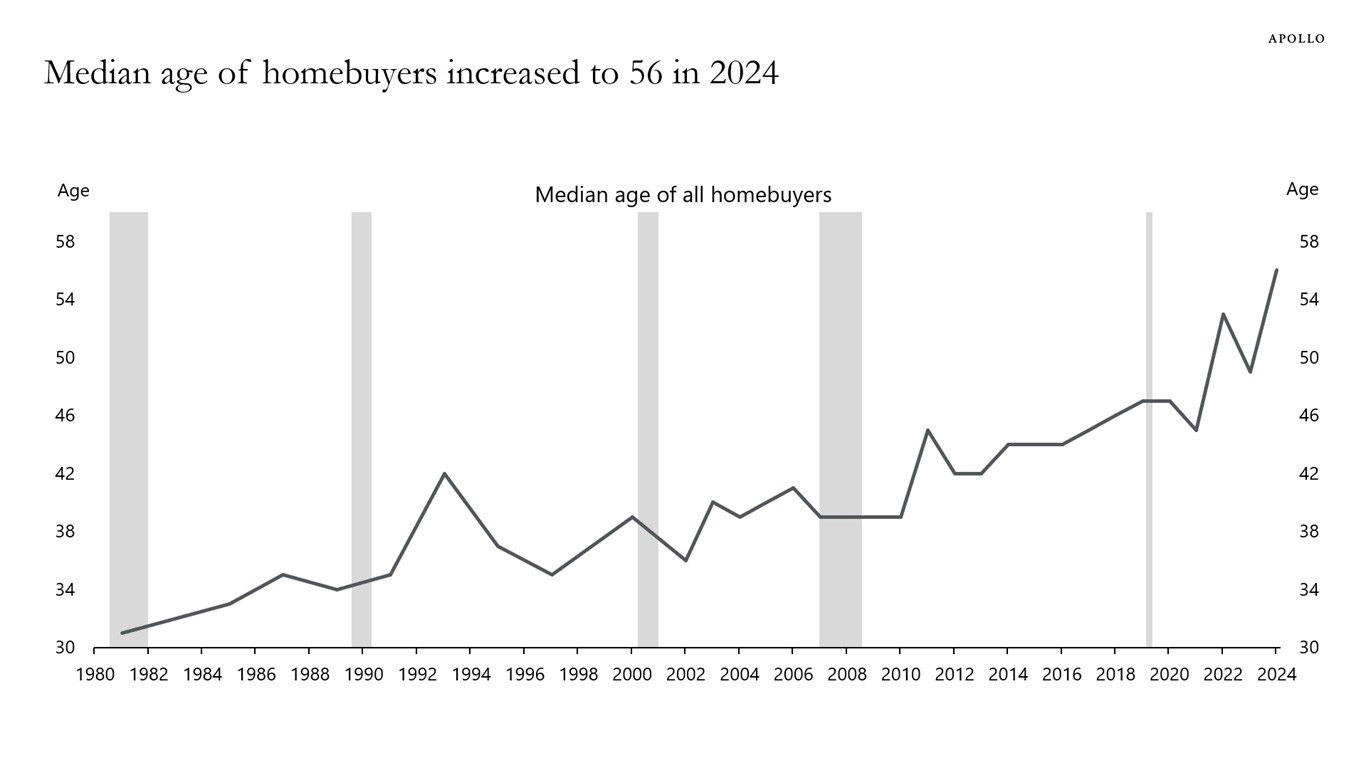

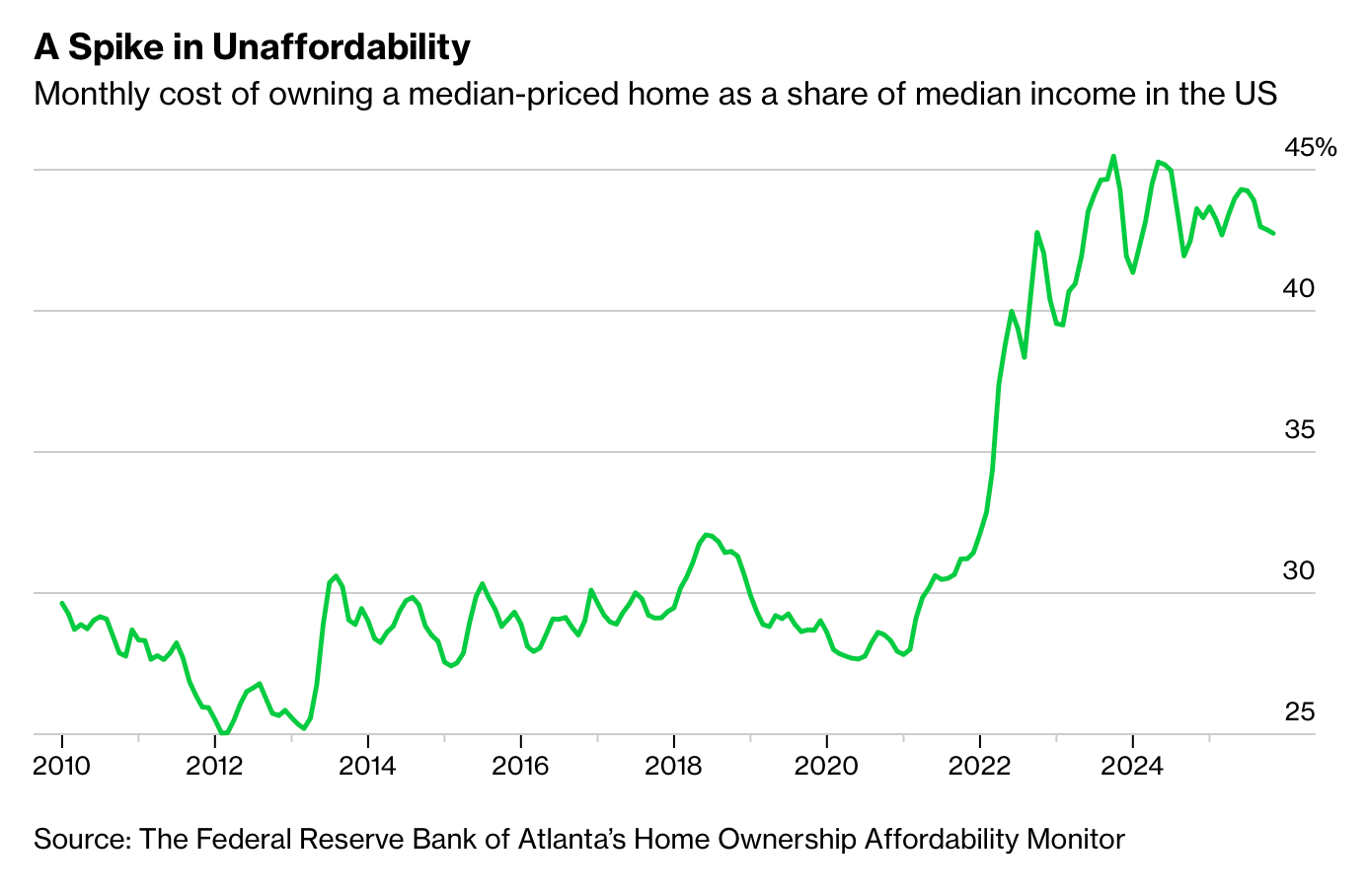

The numbers are almost too bleak to recite. The median age of a first-time homebuyer in the United States hit 56 years old in 2024, up from 45 in 2021 and 31 in 1981. The monthly cost of owning a median-priced American home, as a share of median income, has ballooned from roughly 30 percent a decade ago to nearly 50 percent today. Nearly half of Gen Z agrees with the statement: “No matter how hard I work, I will never be able to afford a home I really love.” Not a mansion. Not a place with a yard. Just a home they love.

This isn’t just a housing problem anymore. It’s a psychology problem, and it’s beginning to show up in the data in ways that should alarm anyone paying attention.

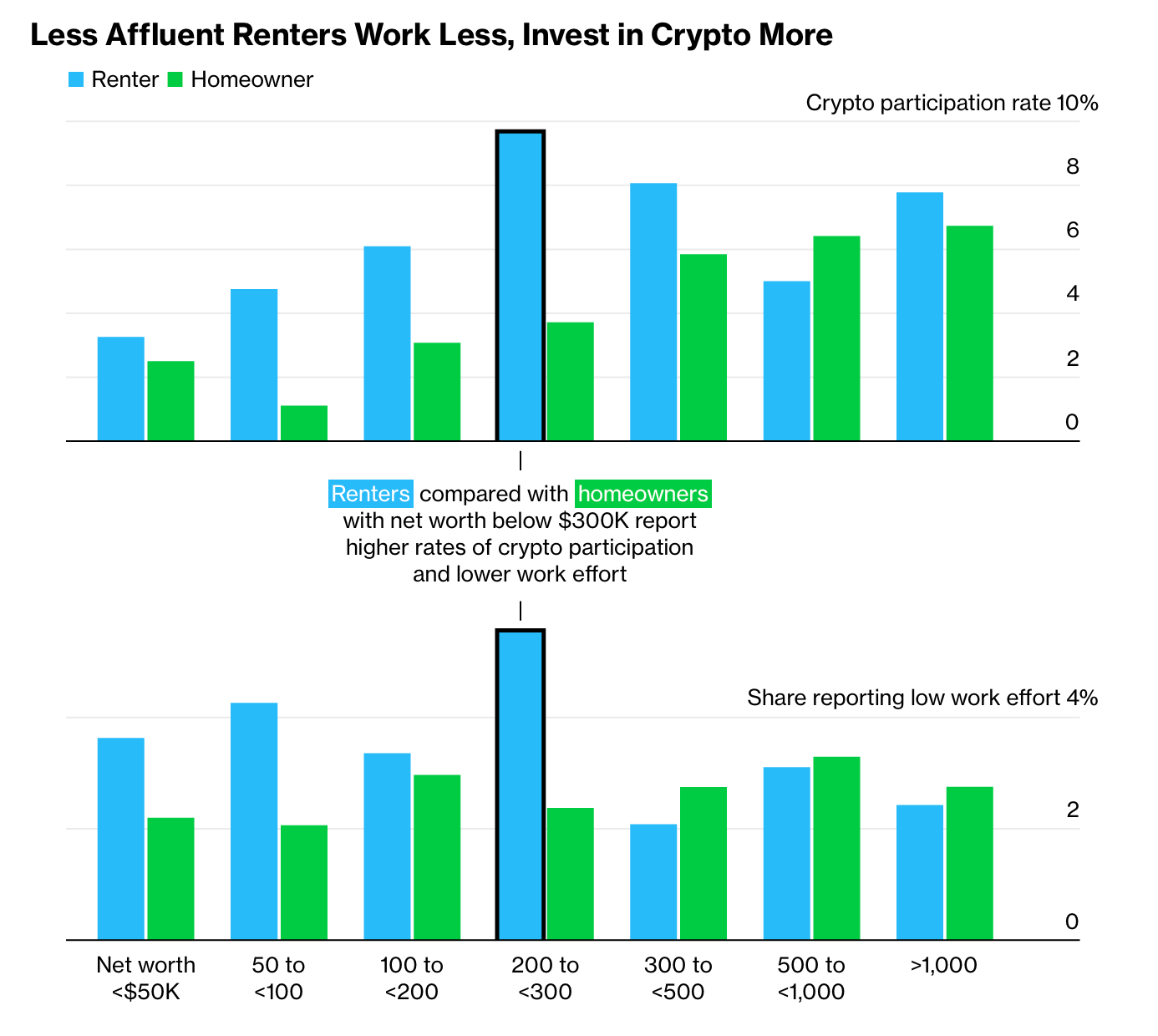

Bloomberg, using the Federal Reserve’s Survey of Consumer Finance data, built a model tracking financial trajectories from age twenty to seventy-five. The findings were stark: people who forgo homeownership end up with significantly less net worth over their lifetimes. That part isn’t surprising — home equity has long functioned as the primary savings vehicle for middle-class families. What was surprising was what people who gave up on homeownership did instead. Renters with net worth under $300,000 reported higher rates of cryptocurrency participation and lower overall work effort than homeowners at comparable wealth levels. The model suggested that “giving up” doesn’t just change where the money goes — it changes how people think about money, work, and the future altogether.

Behavioral economists have a name for the mental state that drives this shift. When people perceive themselves as already operating in the domain of losses, when they believe the baseline outcome is bad, they become dramatically more willing to accept risk. Not because they’re optimistic about the upside, but because the downside already feels like a given.

The money not being saved is flowing somewhere, and it’s not just gambling on crypto and Kalshi. It’s also experiences. The travel industry has documented a sharp surge in what analysts are calling “revenge spending” among younger consumers, but to those doing it, it feels less like revenge and more like a rational reallocation. If the long game is off the table, the short game becomes everything. The dinner, the trip, the concert, the moment — these things are real in a way that a 30-year mortgage increasingly is not. There is something philosophically coherent about this, even if it is also a little heartbreaking.

What makes all of this genuinely dangerous — not just personally, but socially — is what it means for the structures that hold communities together. And here it helps to think about why humans built communities in the first place.

Humans are a species that survived by cooperating. Not metaphorically, but literally — ancestors made it through ice ages and predator-heavy landscapes by hunting in groups, building shelters together, raising children collectively, and maintaining bonds across generations. That cooperation required investment in the future. It required believing that the future was worth investing in. The psychological architecture that made civilization possible, the willingness to sacrifice now for gain later, to plant crops you might not harvest, to build structures you might not live to see completed, was sustained by the belief that you had a stake in what was being built.

Homeownership, for all its complexity as a financial instrument, has historically served as a powerful proxy for that stake. When you own the land you live on, the future is not an abstraction. It’s the garden you’re planning, the school district you’re researching, the neighborhood association meeting you’re slightly annoyed about but still show up to. And when that anchor disappears, something subtle but profound shifts in the way people orient themselves toward time.

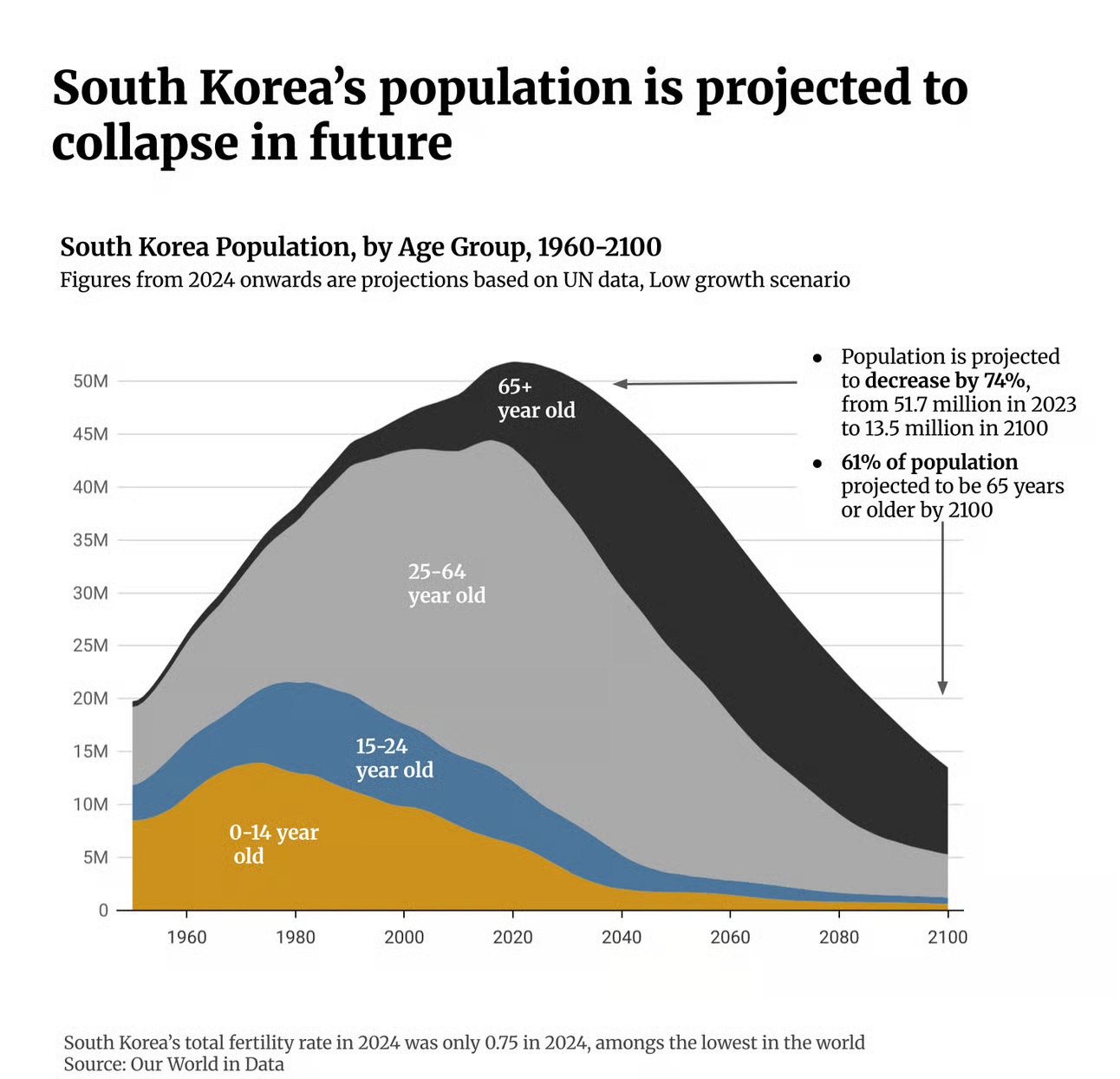

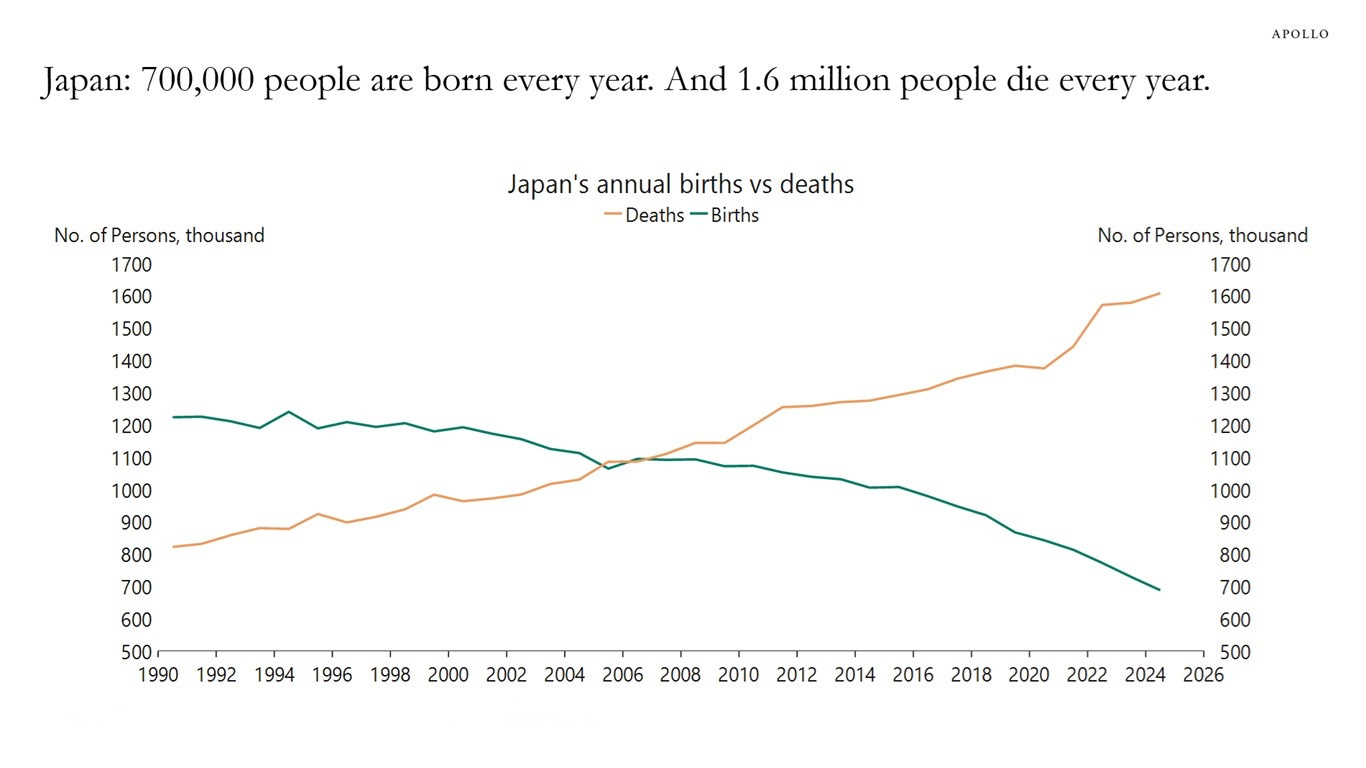

This is not an abstract concern. It is already playing out in real time, most dramatically in East Asia, where the housing affordability crisis is layered on top of brutal working cultures and economic uncertainty in ways that have produced outcomes nothing short of catastrophic.

South Korea’s fertility rate fell to 0.72 in 2023, the lowest ever recorded for any country, anywhere. Japan’s population has been declining for over a decade with no meaningful reversal in sight. China, despite its scale, is projected to lose hundreds of millions of people over the coming century, and its younger generation has coined the term “lying flat” — tang ping — to describe the deliberate choice to stop striving in a system they believe is rigged against them. These are not lazy generations. These are generations that ran the math, didn’t like the answer, and stopped playing a game they had no reasonable chance of winning.

The early signals of the same logic are visible in North America. Marriage rates among Gen Z are down. Birth rates have fallen to historic lows. Polls consistently show that a significant portion of young Americans and Canadians say they are choosing not to have children not primarily for ideological reasons, but because they cannot imagine affording a stable enough life to raise one well. The home — that physical, tangible place that has always anchored the idea of family — has become, for many, a kind of fiction.

The dream was never really just about a house. It was about the idea that effort compounds, that sacrifice means something, that the life you build is actually yours to build. Economies, as much as they run on data, also run on belief — the expectation of inflation shapes inflation; the expectation of growth shapes growth. The same is true of social contracts. When enough people quietly conclude that the contract is broken, their behavior changes in ways that make it break a little more, and then a little more, until the idea of repair starts to feel as fantastical as the listings themselves.

The housing supply crisis is not resolving any time soon. Structural shortages, a lack of skilled trades workers, restrictive zoning, decades of underbuilding, mean that meaningful relief is likely a generation away at minimum. In the meantime, a generation of people who should be planting their feet into the ground are floating, spending, gambling, checking out, and quietly mourning something they were promised and never received.