The Price of Luxury

Nowadays people know the price of everything and the value of nothing

Most people reserve their admiration for rock stars or rocket scientists. Mine belongs to a seamstress. Coco Chanel — orphaned at eleven, raised among nuns, schooled in the austere geometry of need — went on to build one of the most recognisable brands on earth. That trajectory, from threadbare beginnings to the summit of Parisian elegance, has always struck me as the most compelling story in fashion.

Chanel’s genius lay in a deceptively simple conviction: that luxury ought to serve the woman wearing it, not the other way around. The little black dress, the collarless tweed suit, the liberation from corsetry, each was an act of quiet rebellion dressed up as good taste. With the financial backing of wealthy patrons, she opened her first shop in Paris in 1910, selling millinery under the name Chanel Modes. What followed was a career spent stripping fashion of its ornamentation and replacing it with something rarer — functionality in service of grace.

It is bittersweet, then, to observe what the luxury industry she helped pioneer has become.

In the wake of the Covid-19 pandemic, a peculiar frenzy gripped the consumer economy. Flush with stimulus cheques and savings accumulated during months of enforced idleness, shoppers embarked on what became known as “revenge spending,” a cathartic binge that disproportionately favoured luxury brands. For a brief, dizzying moment, Bernard Arnault, chairman of the luxury conglomerate LVMH, ascended to the title of the world’s richest man. The champagne, it seemed, would never stop flowing.

But much of the industry’s windfall came not from selling more, but from charging more. The numbers are staggering. Prada’s Galleria Saffiano bags rose 111% between October 2019 and April 2024. Louis Vuitton’s canvas Speedy bags doubled in the same window. These were not incremental adjustments for inflation; they were audacious bets that desire would outrun arithmetic.

For a time, it did. Then it didn’t.

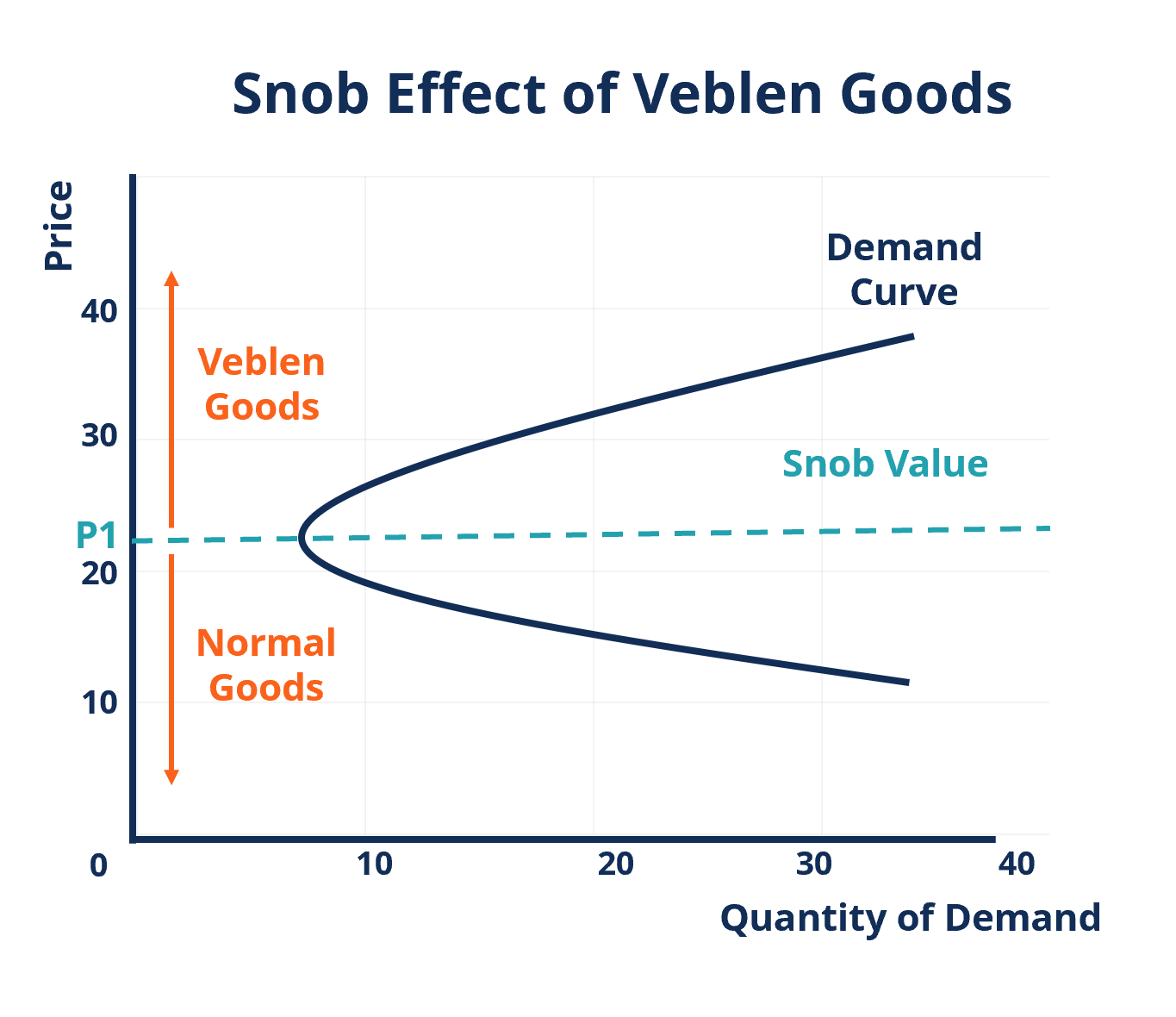

As consumers in the world’s two largest economies, the United States and China, have confronted economic headwinds, demand for luxury goods has fallen sharply. LVMH’s shares have dropped as much as 40% from their 2023 peak and continue to face downward pressure. Burberry and Dior have seen their valuations halved. The steepest decline, however, belongs to Kering, the parent company of Gucci, where industry-wide malaise has been compounded by the brand’s own faltering relationship with its customer base. It turns out that even Veblen goods, those paradoxical products whose allure is supposed to intensify as their prices climb, have a breaking point.

The economic theory behind luxury pricing is elegant in its counterintuitiveness. Thorstein Veblen posited that for certain goods, rising prices thin the ranks of ownership and thereby amplify desirability. A Chanel bag at twice the price is not merely more expensive; it is, in theory, more exclusive, and therefore more coveted. Just imagine if Walmart had doubled the price of everything on its shelves within five years — there would be riots. But luxury operates by a different logic, one in which higher prices are not a deterrent but an invitation.

This logic held for decades, but the recent price escalation has exposed its fragility. The issue, as Katherine Zarrella argued in her New York Times piece on the subject, is not that prices rose, but that they rose without any corresponding improvement in quality or service. Stitching grew looser. Hardware tarnished faster. Customer service became perfunctory. Consumers with deep pockets, the very clientele luxury brands cannot afford to alienate, began asking the most dangerous question a luxury house can face: is this actually worth it?

And there is a more fundamental problem. The Veblen principle functions on scarcity, yet there is nothing scarce about a Louis Vuitton monogram bag when you encounter one every other block in Manhattan or Shanghai. When ubiquity replaces exclusivity, the justification for doubling a price tag within two years evaporates, especially when the target demographic is not the billionaire class, but the aspirational middle class.

Against this backdrop of industry-wide decline, one house has not merely survived but flourished. Hermès posted a 15% sales increase in 2025, even as the S&P Global Luxury Index fell more than 20% the year prior. The answer lies in discipline. Where competitors chased volume, Hermès guarded its supply chain with near-obsessive control. Price increases have been measured, roughly 6–7% per year, rather than the explosive surges favoured by rivals. And the company has remained ruthlessly selective about who can buy its most coveted products. A Birkin bag is not merely expensive; it is genuinely difficult to obtain. The scarcity is not a marketing posture. It is architectural. It is also worth noting that Hermès remains majority-controlled by its founding family, a governance structure that insulates the brand from the quarterly earnings pressures that have driven so many competitors into short-termist excess.

For the consumers priced out, or, perhaps more accurately, who have priced themselves out of caring, alternatives have emerged with surprising vigour. Mid-range brands like Coach and Ralph Lauren have enjoyed a striking resurgence, particularly among younger demographics drawn to their balance of heritage and accessibility. Todd Snyder, the menswear label, has grown from $2 million in sales in 2015 to $130 million in 2024, offering a proposition that luxury houses once claimed as their own: genuine quality at a fair price. Then there is the second-hand market. Platforms like The RealReal and Depop have surged in popularity, offering a secondary avenue to luxury that sidesteps the industry’s price inflation entirely. There is a certain irony in this: the very products that brands inflated beyond reason now circulate in resale ecosystems that undercut the new-product market.

Writing about the luxury industry’s predicament carries a tinge of melancholy, particularly for anyone who admires the craft and vision that once defined these houses. The pivot towards short-term earnings, aggressive pricing, expanded product lines, ubiquitous distribution, has eroded the very identity that allowed these brands to command devotion over decades. This applies beyond apparel. Parallel dynamics are visible in luxury automobiles, with Porsche’s diluted exclusivity, and in high-end hospitality, where prices have become absolutely insane.

Zarrella lamented that today, instant gratification and appearances have become more desirable than substance or intrinsic worth. She may be right about the mainstream luxury houses. But the death of conspicuous, logo-heavy luxury has quietly made room for something more interesting. Brunello Cucinelli, whose founder espouses a humanistic philosophy rooted in community and craftsmanship, has thrived precisely because its identity feels earned rather than manufactured. Its cashmere is not merely expensive, it is traceable and dyed and sewn by artisans paid above-market wages.

Oscar Wilde once quipped that people know the price of everything and the value of nothing. He was writing about Victorian society, but he might as well have been diagnosing the modern luxury industry. Perhaps the most useful legacy of its current reckoning is this: a reminder that scarcity and value are not strictly functions of price. Coco Chanel understood this intuitively. She built a brand on the radical premise that elegance should be affordable, functional, and honest. The industry she helped create forgot that lesson. Some, at least, appear to be remembering it.