The Private Credit Implosion

The technology that was supposed to fuel private credit’s golden age may have just triggered its biggest crisis since the global financial crisis.

Imagine you run a mid-sized software company. You need capital to grow, but the banks say no — your business is too risky, too small, or doesn’t fit neatly into their lending criteria. Where do you go?

Increasingly, the answer has been private credit: investment funds that step in where traditional banks won’t, offering loans to businesses that fall outside the conventional banking system. Over the past decade, private credit has grown from a niche corner of finance into a multi-trillion-dollar industry, filling a gap that banks left open after tightening their lending standards in the wake of the 2008 financial crisis. This matters beyond Wall Street. Private credit funds the companies that employ people, build infrastructure, and develop technology. When private credit is healthy, capital flows to businesses that need it. When it isn’t, the effects ripple outward — into jobs, into pensions, and into the broader economy.

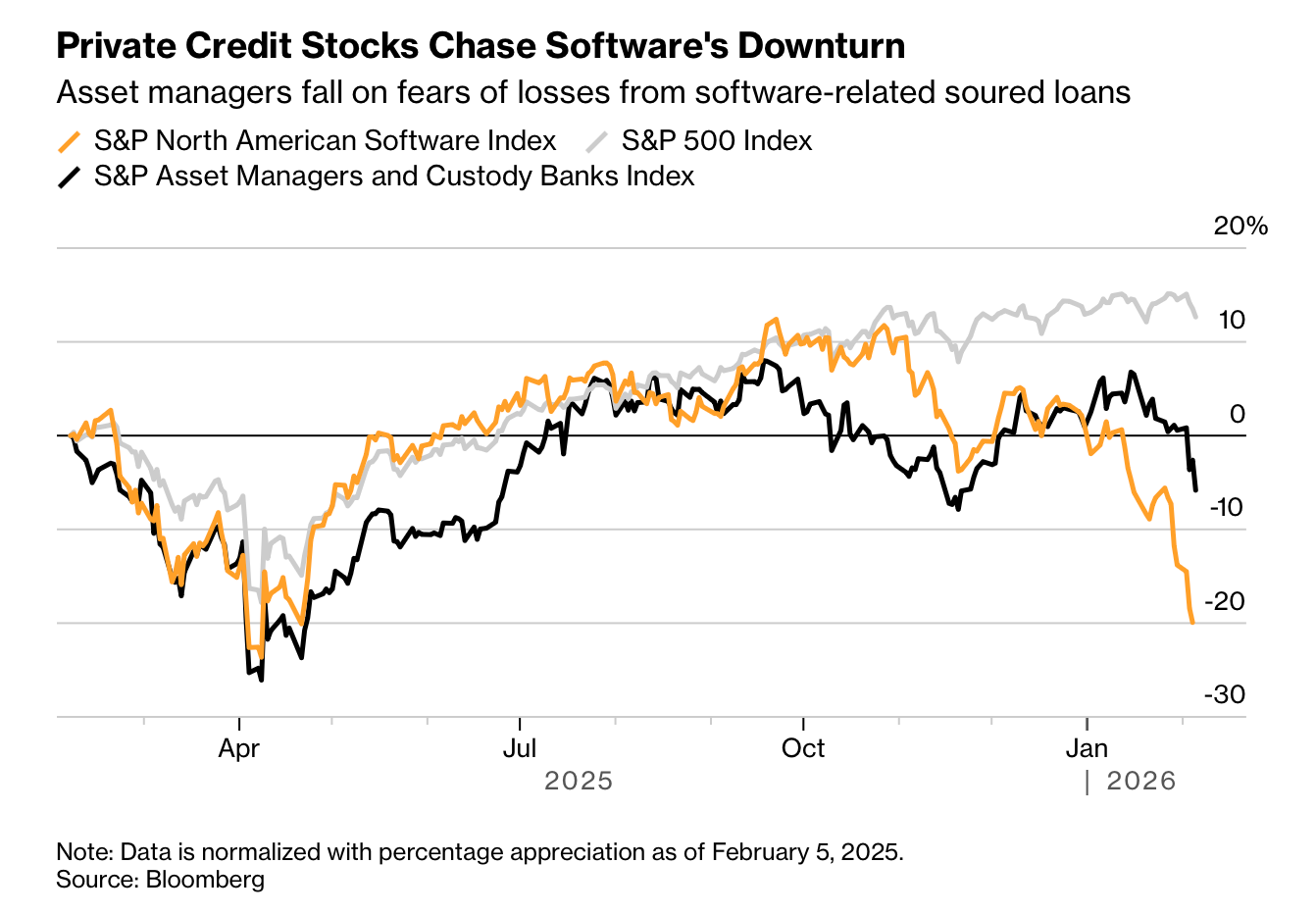

Last summer, private credit was the talk of the financial world. The explosion of investment in artificial intelligence had created an enormous appetite for capital — companies needed billions to build data centers, develop models, and scale infrastructure. One of the marquee deals was Blue Owl Capital’s $27 billion arrangement with Meta to finance data center construction in Louisiana. It was the kind of headline that signaled private credit had arrived as a dominant force in modern finance.

But even at the peak, there were warning signs. Conversations with investment professionals at the time revealed a shared unease: the space was getting crowded. More funds were entering, competition for deals was intensifying, and the pressure to deploy capital meant that underwriting standards — the rigor with which lenders evaluate borrowers — were beginning to slip. The consensus was that “dispersion” would define the industry going forward. Some funds would thrive, but others, the ones that cut corners to win deals, would eventually pay the price.

The test came sooner than anyone expected, and ironically, it came from AI itself — the very force that was supposed to propel the industry to new heights. Earlier this year, Anthropic’s release of Cowork and its suite of AI agents sent a shockwave through financial markets. The concern was straightforward but devastating. If AI agents could automate much of what traditional software companies sell — customer support, data analysis, workflow management — then the business models underpinning thousands of software firms were suddenly in question. These companies largely rely on selling subscriptions on a per-seat basis: the more employees a client has, the more they pay. AI threatens to replace that model with one based on token consumption, where a single AI agent could do the work of many seats at a fraction of the cost.

The public markets reacted swiftly. The IGV software ETF fell more than 15% year to date. High-quality companies like Intuit dropped over 30%, not because their businesses had collapsed, but because investors feared they would. The second-order effects hit private credit hard. Many of the companies in private credit portfolios are exactly the kinds of mid-market software firms most vulnerable to this disruption. And because private credit funds don’t trade on public exchanges the way stocks do, the stress didn’t show up immediately in prices. It showed up in something more dangerous: redemptions.

A Slow-Motion Bank Run

To understand why redemptions are so dangerous for private credit, you need to understand how these funds value their assets, and why that process is fundamentally different from public markets.

Here’s a simplified example. Say a private credit fund lends $100 to a software company for five years at 8% interest. The fund records this loan as a $100 asset on its books. The next day, fears about AI disruption cause the market to demand higher interest rates from similar software companies — say, 8.5% instead of 8%. What is that loan now worth?

In public markets, the answer is clear, roughly $98. When market interest rates go up, the value of existing lower-rate debt goes down. If you sold the note today, the buyer would need a discount to achieve the new market rate of 8.5%. This is called “mark-to-market” — valuing your assets at what the market would actually pay for them right now.

But private credit funds don’t have to play by these rules. A fund manager might reasonably argue: “Nothing has changed with the borrower. They’re still making payments. I’m not selling the loan. It will pay $100 at maturity plus interest. Why would I mark it down to $98 based on market sentiment that might reverse tomorrow?” This is called “mark-to-model” — valuing assets based on an internal assessment rather than market prices. Both approaches have legitimate uses. But the tension between them creates a dangerous vulnerability.

Many of the largest private credit firms run retail-facing vehicles called business development companies (BDCs). Some of these BDCs allow investors to redeem their shares — not whenever they want, but in limited amounts, typically once per quarter. Crucially, these redemptions happen at net asset value, which is based on the fund’s own marks. If a fund says its loans are worth $100 but the market believes they’re worth $98, investors have a powerful incentive to redeem. They can cash out at $100 for something they believe is worth only $98, a built-in arbitrage. And once some investors start redeeming, others follow, fearing they’ll be left holding assets that are worth even less once the selling pressure hits.

This is the dynamic that has been playing out across the private credit industry in recent months. Redemption requests have surged to historically high levels. Some funds have been forced to limit withdrawals, creating scenes uncomfortably reminiscent of the Silicon Valley Bank run — except this time it’s happening in private markets, where there’s less transparency and fewer safety nets. The very act of restricting redemptions can accelerate the panic. When investors hear that a fund is gating withdrawals, it confirms their suspicion that the assets aren’t worth what the fund claims. Trust erodes, and the cycle intensifies.

Leverage makes all of this worse. Many private credit funds borrow money from banks to boost their returns, using their loan portfolios as collateral. This works well when asset values are stable. But when values start to fall — or when banks suspect they might — lenders can issue margin calls, demanding that funds post additional collateral or pay down their borrowings. To meet those calls or fund redemptions, managers may need to sell assets. But selling illiquid private loans at a discount further depresses valuations, which triggers more margin calls and more redemptions. It’s the same doom loop that has brought down financial institutions throughout history, from Long-Term Capital Management in 1998 to Bear Stearns in 2008.

Why This Matters Beyond Wall Street

The private credit crunch is not happening in isolation. It follows the high-profile bankruptcy of subprime auto lender First Brands and the collapse of auto-parts company Tricolor — losses significant enough that investors have filed lawsuits against Jefferies, which was involved in lending to First Brands. These events are testing an industry that has enjoyed an almost uninterrupted run of growth since the financial crisis.

The implications extend well beyond the investors in these funds. For the broader economy, private credit is now a major source of financing for mid-sized businesses. If funds become more cautious or pull back lending, companies that rely on this capital — for payroll, for expansion, for operations — could find themselves squeezed. That translates into slower growth, hiring freezes, or layoffs.

For retirement savings, many pension funds and insurance companies have allocated heavily to private credit in search of higher returns. If these investments underperform, it could affect the retirement security of millions of people who have never heard of a BDC. And for the financial system at large, the interconnection between private credit funds and traditional banks through leverage creates channels for contagion. Stress in private credit doesn’t stay contained in private credit.

This isn’t the end of the industry. Private credit serves a genuine economic need — channeling capital to borrowers that banks can’t or won’t serve — and that need isn’t going away. But the current turbulence will reshape the landscape. The funds that underwrite carefully, maintain conservative leverage, and communicate honestly with investors about their marks will emerge stronger. Those that stretched for yield, overleveraged, or relied on opaque valuations to mask deteriorating portfolios will not. The “dispersion” that industry insiders warned about last summer is no longer a prediction. It’s happening now.

The lesson for investors and observers alike is an old one, made new by modern finance: when the price of something is hard to see, it’s easy to pretend it hasn’t changed. But pretending doesn’t make it so — and eventually, reality catches up.