What the Iran War Reveals About Energy, the Gulf, and Wall Street

Two Losers and a Winner

There is a running joke on the internet that President Trump has a calendar of foreign leaders he intends to take down each month in the lead-up to the midterms—almost comical, as if he is collecting Pokémon. In January, the United States through a swift military operation captured Maduro, the leader of Venezuela. In February, the U.S. assisted the Mexican government in eliminating the cartel leader known as “El Mencho.” And as March arrived, President Trump launched what is effectively a war under Operation Epic Fury, killing the Iranian Supreme Leader Ali Khamenei during the opening wave of airstrikes.

With each operation, the magnitude of response has escalated. The capture of Maduro was drama-free and broadly popular. The killing of El Mencho sparked a sharper backlash, as cartels attacked airports and burned vehicles across parts of Mexico, stranding tourists and cancelling flights. The most significant response, by far, has come from Iran, which launched hundreds of ballistic missiles and drones against Gulf states including the United Arab Emirates, Kuwait, Qatar, and Saudi Arabia, and effectively shut down the Strait of Hormuz, through which roughly 20% of the world’s oil and gas supply passes.

While at the time of this writing, Mr. Trump has signaled that the war may be reaching its conclusion, telling CBS News the conflict is “very complete, pretty much”—the world is much different than it was before a week of fighting between the U.S. and Israel against Iran. To explore the implications, I want to play a game called Two Losers and a Winner, inspired by the classic icebreaker of two lies and a truth.

The First Loser: Energy-Dependent Nations

The first and perhaps the most glaring takeaway is that hydrocarbons remain foundational as an energy source for nearly every country on earth. Oil and gas power industries from manufacturing to transportation, agriculture to electricity generation. To become economically secure, a country must first consider how to become energy secure, much as the Covid-19 pandemic taught the world the importance of securing domestic supply chains for critical industries. Without energy security, countries remain hostage to a fragile global supply chain, vulnerable at a handful of strategic chokepoints.

The Strait of Hormuz is the most consequential of those chokepoints. It is a narrow waterway just 21 miles wide at its narrowest point, separating Iran and Oman, through which approximately 20 million barrels of oil pass each day, roughly one-fifth of global seaborne oil trade. An estimated 84% of crude shipments through the strait are destined for Asian markets, with China, India, Japan, and South Korea accounting for nearly 70% of those shipments, according to the U.S. Energy Information Administration. Europe, too, depends on the strait, as roughly 30% of the continent’s jet fuel supply originates from or transits through it, and about 12–14% of Europe’s liquefied natural gas (LNG) comes from Qatar via this corridor.

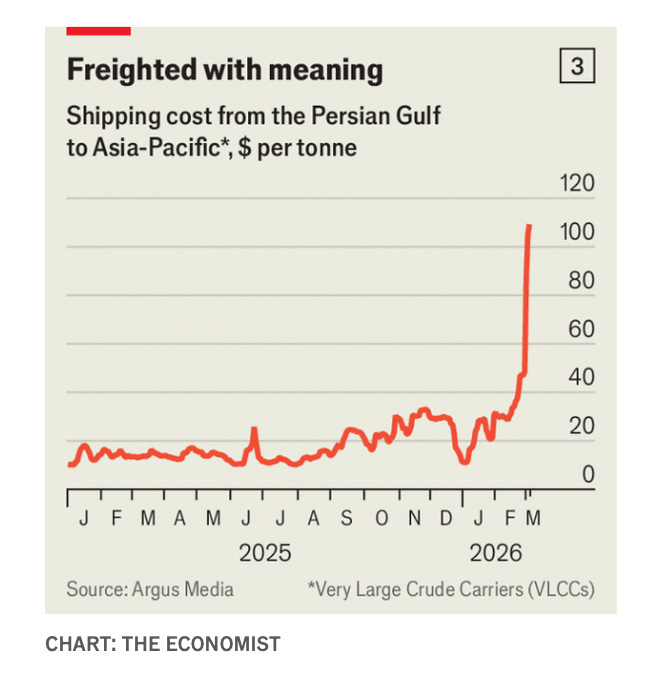

The conflict exposed this dependency with brutal clarity. Within days of Operation Epic Fury, tanker traffic through the strait collapsed by roughly 70% before falling to virtually zero, as the Islamic Revolutionary Guard Corps declared the strait closed and threatened to set ablaze any vessel attempting passage. Over 150 ships anchored outside the strait, unwilling to enter. Insurance premiums for very large oil tankers surged by hundreds of thousands of dollars per transit. Brent crude, which traded around $70–73 per barrel before the war, spiked above $100 per barrel for the first time since Russia’s 2022 invasion of Ukraine, hitting an intraday high near $120 before settling around $99. U.S. gasoline prices jumped roughly 17% within a week of the war’s start, with analysts warning of $4–45 per gallon if the strait remained closed.

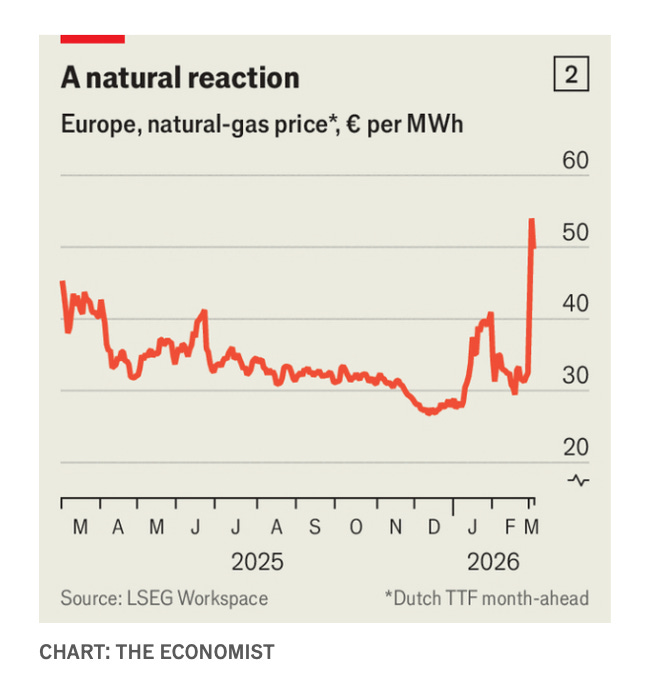

The LNG market was hit just as hard. On March 2, Qatar, the world’s largest LNG exporter, announced it had halted all gas production after Iranian drones struck Qatari gas facilities, and declared force majeure on its gas contracts two days later. European natural gas prices nearly doubled in the aftermath. Goldman Sachs Research estimated that a hypothetical two-month disruption of LNG supply through the strait could push European natural gas prices above €100 per megawatt-hour, compared to roughly €32 before the war. Qatar’s energy minister warned that if the war continued, other Gulf producers could be forced to halt exports, which “will bring down economies of the world.”

The downstream effects on developing nations are catastrophic. I witnessed this dynamic firsthand in Sri Lanka in 2022, in the wake of the Covid-19 pandemic. The country’s rampant fiscal expansion had led to surging inflation and economic stagnation. One of the core drivers was the inability to import energy at affordable prices. As the Sri Lankan rupee collapsed, the cost of fuel imports soared, dragging down agriculture, transportation, and manufacturing. During my visit to the urban slums of Colombo, many workers were unable to commute because the cost of transportation had become unaffordable. Families struggled to make ends meet, and many turned to crime—theft, robbery, and even trafficking of crystal methamphetamine. Trust within communities eroded. Children were pulled from schools, unable to afford basic supplies. These consequences set the nation back by decades.

The same dynamics now threaten countries across Asia. Japan’s refiners, who source roughly 95% of their crude from the Gulf, have already asked the government to release stockpiled oil. Pakistan, which sources 99% of its LNG imports from Qatar, faces an acute crisis. India and China, while more diversified, are still deeply exposed. The IMF has warned that if oil prices remain above $100 per barrel for a sustained period, it could shave 0.4 percentage points off global GDP growth and add 1.2 percentage points to inflation.

The world’s dependence on hydrocarbons, particularly in emerging markets, is often glossed over as media outlets advocate for cleaner alternatives like wind, solar, and nuclear. While diversifying energy sources is essential, this conflict has again demonstrated that the world remains deeply reliant on oil and gas—and that for developing nations, a lack of access to cheap energy is not merely an inconvenience but a direct path to economic and social turmoil.

The Second Loser: The Gulf States

For the past decade, Gulf states, particularly the UAE and Qatar, have invested enormous effort in transforming their economies away from a singular dependence on hydrocarbons. Dubai has become synonymous with luxury tourism, financial services, and architectural ambition. Qatar hosted the 2022 FIFA World Cup. Saudi Arabia has poured billions into entertainment, sports, and its Vision 2030 diversification agenda. More recently, the UAE has positioned itself as a hub for artificial intelligence and technology. The pitch to the world was clear: the Gulf is stable, modern, and open for business.

The war with Iran shattered that narrative. Within hours of Operation Epic Fury, Iran launched retaliatory strikes across the entire Gulf Cooperation Council. The UAE alone reported facing 174 ballistic missiles, over 680 drones, and eight cruise missiles in the initial waves. While the vast majority were intercepted, the debris and the projectiles that got through inflicted real damage. Dubai International Airport, the busiest airport in the world for international traffic, was struck and temporarily shut down, stranding roughly 20,000 passengers in the UAE alone and another 8,000 in Qatar. A drone struck near the Fairmont Hotel on Palm Jumeirah, one of Dubai’s most iconic luxury destinations. The Burj Al Arab and Jebel Ali Port were damaged by falling intercept debris. An Amazon Web Services data center caught fire after being hit. Four people were killed in the UAE, foreign workers from Pakistan, Nepal, and Bangladesh, and over 100 were injured.

The images of smoke rising over Palm Jumeirah and yachts sailing past burning port facilities struck at the heart of the Gulf’s brand. As one analyst observed, seeing Dubai and Doha bombed is as jarring for the region as seeing Miami or Seattle bombed would be for Americans. For a region that has attracted the world’s wealthy by projecting safety and stability, this was a fundamental breach of trust. In the days following the strikes, banks reportedly began offering employees relocation packages away from the region. Airlines including Emirates, Etihad, and Qatar Airways, which together operate over a thousand flights daily, suspended operations entirely.

This is not to say that companies will abandon the region altogether. The Gulf’s infrastructure, tax advantages, and geographic positioning remain compelling. But the war has forced businesses, investors, and wealthy individuals to price in geopolitical risk in a way they previously did not. The plan for the region to become a global hub for entertainment, finance, and technology may no longer follow the trajectory its leaders envisioned. Businesses will be more cautious about long-term capital commitments. Tourists and expatriates will weigh safety considerations they once took for granted. While the Gulf states were largely spared during the tit-for-tat exchanges between Iran and Israel in 2024 and 2025, this time a sustained week of fighting has inflicted damage that may prove economically irreversible in the short term.

The Winner: Wall Street

Amid all this destruction and disruption, there is a winner—and, remarkably, it is Wall Street. Once again, markets called Mr. Trump’s bluff and, so far, have largely gotten it right. Despite oil surging past $100, despite a region in flames, the S&P 500 has displayed surprising resilience. On the first trading day of the war, the Dow fell nearly 600 points intraday before recovering to close down just 73 points, while the S&P 500 and Nasdaq actually finished in the green. Even on Monday, March 9, after oil briefly spiked near $120 a barrel, the S&P 500 rebounded from an intraday loss of over 1.5% to close up 0.83% at 6,796 after Trump signaled the war’s end. The Dow, despite its worst weekly decline since April, still managed to recover 239 points on the day.

There are structural reasons for this resilience. The S&P 500 is now heavily concentrated in mega-cap technology and AI companies that are far less exposed to energy prices and physical supply chain disruptions than the manufacturing-heavy index of decades past. Research from Carson Group, which compiled data from 40 major geopolitical events over the past 85 years, found that the S&P 500 has historically lost just 0.9% in the first month following a major geopolitical shock but gained 3.4% over the following six months. Investors also had time to position for this conflict—the military buildup had been well-telegraphed, and Wall Street widely expected a contained, short-duration operation.

This market behavior has become a recognizable pattern under the Trump administration. Since “Liberation Day” in April 2025, when sweeping tariff announcements sent the market down over 10% within weeks, investors have learned to treat each new escalation—threats over Greenland, additional tariffs, now a war—with a degree of skepticism. The market has essentially adopted a “wait and see” posture, betting that disruptions will be temporary and that the administration will de-escalate before permanent economic damage is done.

Yet there are limits to this resilience. The week ending March 7 was the worst combined week for stocks and bonds since the tariff shock last April, as both fell simultaneously, the inflationary shock of an oil supply disruption pushed Treasury yields higher rather than lower, breaking the traditional crisis playbook. JPMorgan’s trading desk turned “tactically bearish” on Monday, warning that a 10% correction from the S&P 500’s peak, down to roughly 6,270, remained possible if the conflict dragged on. The $100-per-barrel oil threshold is widely viewed on Wall Street as the level at which real economic damage begins to compound.

Still, the market’s ability to absorb a hot war with Iran without a major selloff is a testament to the structural strength of American companies—and also, perhaps, a reminder of the limited extent to which the U.S. equity market reflects the broader American economy or the global economy. The S&P 500 is not measuring the pain of stranded tanker crews, Pakistani workers killed by debris in Abu Dhabi, or Japanese refiners scrambling for crude. It is measuring the profit expectations of Nvidia, Apple, and Microsoft. Whether that disconnect is a feature or a flaw depends on your perspective.

Will Next Time Be Different?

In the end, the war in Iran has demonstrated just how fragile and interdependent the global order remains. Geopolitical shocks produce winners and losers, and the distribution of those outcomes is rarely equitable. The conflict in Iran threatens regional stability across Asia, where social unrest is already common, and could derail the Gulf’s ambitious economic transformation. Sustained high oil prices risk stagflation in the United States and could tip developing economies into outright crisis.

As the conflict gradually de-escalates and the first tankers resume passage through the Strait of Hormuz, it is worth asking a simple but uncomfortable question: will next time be different? The answer, almost certainly, is no. So long as the world remains dependent on a handful of narrow waterways for its energy supply, and so long as geopolitical rivalries persist, shocks like these will recur. The only variable is whether countries, and markets, will be better prepared when they do.