What Is Financial Literacy, Really?

Even your parents don't know

You’re scrolling through TikTok and someone’s dead serious explaining how you can “hack” your credit card by just paying the $10 minimum payment each month because “it’s basically free money until next month.” You immediately burst out laughing. So much for #FinTok and #FinancialLiteracy. Then your mom texts asking if you’ve started your retirement fund yet, even though you’re still paying off that laptop you had to put on a credit card last year. You close the app feeling somehow confused because honestly, what’s the point of saving when a studio apartment rent costs almost as much as your entire paycheck?

The confusion you feel isn’t actually your fault. It turns out that even the experts can’t agree on what financial literacy actually means, and that matters more than you think. Because if we can’t define it, how are we supposed to achieve it? And more importantly, how is anyone supposed to teach it?

I spent an hour reading a research paper called “Defining and Measuring Financial Literacy” published by RAND, a policy think tank. The paper was written by Angela A. Hung, Andrew M. Parker, and Joanne Yoong in 2009, and it performed what’s called a meta-analysis, which is basically when researchers look at a bunch of other research to find patterns and problems. What they found was pretty wild: everyone from government agencies to banks to academics was using the term “financial literacy” to mean completely different things. Some thought it meant knowing what compound interest is. Others thought it meant actually saving money. Nobody could agree, and that’s a massive problem when we’re trying to figure out why so many people struggle with money.

Understanding financial literacy matters because the decisions we make about savings, spending, and investing don’t just affect us today—they shape our entire lives. Research in behavioral economics has shown that people typically don’t make optimal financial decisions, which isn’t exactly shocking news to anyone who’s ever impulse-bought something at 2 AM. But here’s what is shocking: back in 2004, only half of adults who were close to retirement age could correctly answer basic questions about inflation and compound interest. Mind you, these are people who’ve been managing money for decades.

So clearly, financial literacy is both important and lacking. But before we can fix the problem, we need to understand what we’re even talking about. Most people think financial literacy and financial knowledge are the same thing, but they’re not. Financial knowledge is just understanding financial products and services—knowing what a mortgage is, what an ETF does, how credit cards work. It’s information.

Similarly, financial literacy isn’t the same as financial attitude, which is basically your underlying feelings and preferences about money. Some people are naturally more risk-averse, others are comfortable with uncertainty. Those are preferences that shape how you approach money, but they can’t be judged as right or wrong the way knowledge can.

The President’s Advisory Council on Financial Literacy, which was convened specifically to improve financial literacy among Americans, defines it as the ability to use knowledge and skills to manage financial resources effectively for a lifetime of financial well-being. It’s behaviorally focused—did you actually do the thing you were supposed to do?

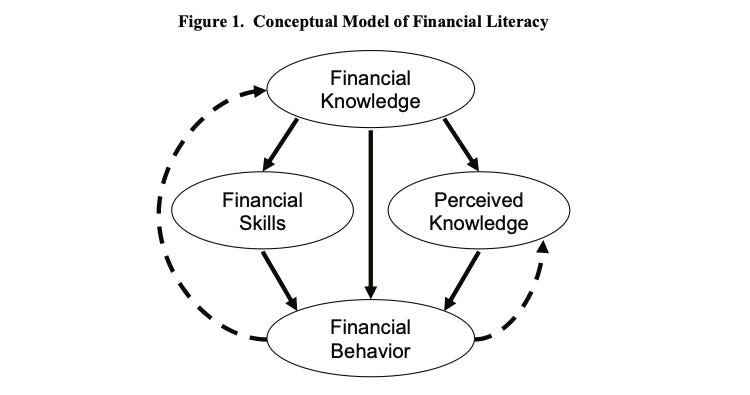

Hung, Parker, and Yoong argue that’s too narrow and doesn’t help us understand how to actually improve financial literacy. They propose we think of it as a combination of financial knowledge, skill, and behavior, along with how all these things interact with each other. They created a composite definition: “knowledge of basic economic and financial concepts, as well as the ability to use that knowledge and other financial skills to manage financial resources effectively for a lifetime of financial well-being.”1 In this framework, financial knowledge is just the starting point, the most basic form of literacy. Actual financial literacy depends on what you know, what you think you know, the skills you’ve developed, and the experience you’ve gained through actually managing money in the real world.

Think about it like learning to drive. Someone can explain how a car works, teach you the rules of the road, and show you what all the pedals do. That’s knowledge. But you’re not actually a competent driver until you’ve been behind the wheel in different conditions—rush hour traffic, bad weather, that one intersection in your neighborhood where nobody follows the rules. Financial literacy works the same way. It’s not a static thing where someone teaches you to budget and save and boom, you’re done. It’s dynamic and constantly evolving based on your circumstances.

Let’s say you’re saving for your first car. You’ve got a plan, you’re putting money away each month, you’re doing everything right. Then you have to buy a last-minute plane ticket because a family member is sick. Suddenly your car fund takes a hit. That’s not a failure of financial literacy—that’s life. The literacy part is being able to adapt, to reassess, to figure out how to keep moving toward your goal even when circumstances change. It’s the accumulated experience of managing money under pressure, making trade-offs, and learning from the choices you make.

Each time you navigate one of these situations, you’re building actual financial literacy, not just knowledge. And what’s fascinating is that the experience feeds back into your knowledge base. The next time you face a financial decision, you’re drawing not just on what you were taught, but on what you’ve lived through. It’s a cycle—behavior creates experience, experience shapes knowledge, knowledge influences future behavior.

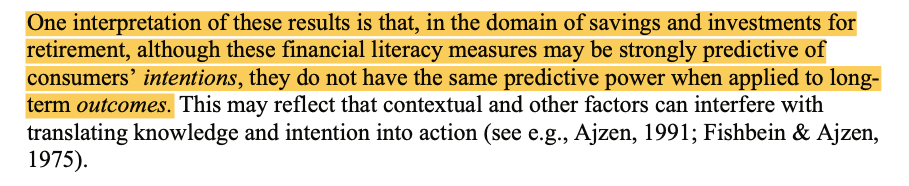

Here’s something else the research shows that’s both validating and slightly unsettling: financial literacy predicts people’s planning behavior—their intentions about what they should do with their money—but it doesn’t actually predict what their behavior will be. In other words, even if you fully intend to save that money, transfer it to your high-yield savings account, and not touch it, there’s still a good chance you won’t follow through. Life happens. Temptation happens. Emergencies happen. But the good news is that financial literacy does improve that planning process. It increases the likelihood that you’ll follow through, even if it doesn’t guarantee it. Think of it as shifting the odds in your favor rather than providing a foolproof system.

And here comes the most interesting part: what you think you know matters almost as much as what you actually know. The research found that perceived knowledge—your confidence in your financial understanding—predicts financial behavior independently of actual knowledge. People who feel confident about their financial decisions tend to make different choices than people who doubt themselves, even when their actual knowledge levels are similar. In fact, when researchers measured the correlation between what people actually knew and what they thought they knew, it ranged from extremely weak (.10) to fairly strong (.78), with a median correlation of .49. That means perceived and actual knowledge are related, but they’re far from the same thing.

This is actually liberating when you think about it. You don’t need to have everything figured out before you start making financial moves. Having some confidence—even if it’s not perfectly calibrated to your actual knowledge—can get you to take that first step. Maybe you open that retirement account even though you’re not entirely sure how to allocate your investments. Maybe you start budgeting even though you don’t know all the “optimal” strategies. That action creates experience. And experience, even when it includes mistakes, feeds back into your actual knowledge. You learn what works, what doesn’t, what you need to research more. The process itself builds literacy.

But here’s the important caveat: this only works if you’re somewhat grounded in reality. People consistently overestimate their financial knowledge—we think we know more than we actually do, and this pattern shows up across virtually every domain, not just money. So while a baseline level of confidence helps you take action instead of being paralyzed by uncertainty, overconfidence can lead you to make moves without understanding the consequences. It’s the difference between opening a high-yield savings account because you’re pretty sure it’s better than a regular one (good confidence) versus putting your entire emergency fund into a risky investment because you saw someone on TikTok say it’s a sure thing (dangerous overconfidence).

The sweet spot is having enough confidence to act, enough humility to know you don’t know everything, and enough curiosity to learn from what happens next. You’re building financial literacy through doing, not waiting until you’re perfectly educated to start.

This brings us back to the generational tension that probably prompted you to think about this in the first place. Your parents tell you to save, to avoid debt, to invest wisely. That’s financial knowledge, and it’s not wrong. But it’s not complete financial literacy either, because the financial landscape they learned to navigate is fundamentally different from yours. They might lecture you about ‘risky’ new investment apps like Coinbase, not understanding that the tools available to you—from fractional shares to new types of ETFs to decentralized finance—didn’t exist when they were your age. The housing market, the job market, the cost of education, the entire economic context has shifted. Their knowledge isn’t useless, but it’s not automatically applicable to your situation either.

So what does all this mean practically? It means that financial literacy isn’t something you either have or don’t have. It’s not a destination you reach and then you’re done. Instead, it’s an ongoing process of developing and updating your financial knowledge to keep pace with changing markets and products, applying that knowledge as skills in real situations, and building good financial behaviors and habits over time. You’re not going to get it right on the first try. Intention doesn’t guarantee results. But consistency leads to progress, and progress leads to results.

The social media narrative about Gen Z and money tends toward extremes—either we’re irresponsibly lavish, blowing our paychecks on avocado toast and designer water bottles, or we’re neurotically frugal, haunted by economic anxiety and convinced we’ll never retire. The truth is messier and more human than either caricature. We’re learning to navigate a financial system that’s more complex than ever, with more choices and more risks than previous generations faced, often without adequate education or support. And we’re doing it while being constantly bombarded with conflicting messages about what we should be doing with our money.

So if you spent $200 at Lululemon or splurged on brunch at that new spot everyone’s talking about, don’t spiral into guilt. But do remember that financial literacy is behavioral, which means it improves with practice. Every financial decision you make, whether it works out perfectly or teaches you something the hard way, is building your literacy. The goal isn’t perfection. It’s getting incrementally better at understanding your financial reality, making informed choices, and adapting when things don’t go according to plan. That’s what financial literacy actually means, and that’s something even your parents are still working on, whether they admit it or not.

Hung, Angela A., Andrew M. Parker, and Joanne K. Yoong. 2009. “Defining and Measuring Financial Literacy.” RAND Working Paper WR-708. Santa Monica, CA: RAND Corporation.

"Actual financial literacy depends on what you know, what you think you know, the skills you’ve developed, and the experience you’ve gained through actually managing money in the real world." Love that!