Why Does Gold Price Keep Going Up?

Maybe your parents were right all along

Picture this. It’s Christmas dinner. Your dad’s smirking over the turkey. Your mom’s giving you that look. They’ve been telling you for years to buy gold and hold it forever. You rolled your eyes and told them Bitcoin is the future, that they don’t understand digital assets, that they’re stuck in the past.

This year? They have the receipts. Gold is up over 50% while Bitcoin has been basically flat. And now they won’t let you forget it.

But here’s the thing—this isn’t just about your parents being right (though they definitely are). Something fundamental is happening with gold right now, and it’s revealing a shift in how the global economy works that affects all of us. Even companies like Wealthsimple, the poster child of fintech innovation, just added gold buying to their platform. When the digital-first generation starts hoarding physical metal, you know something’s changed.

So what’s actually going on? Why is everyone suddenly loading up on gold?

Gold’s real superpower isn’t protecting you month-to-month. It’s that over the long term, it retains value in ways other assets can’t. And that creates this strange psychological effect: because we know gold holds value over decades, we expect it to protect us right now, so presumably people buys gold during times of uncertainty.

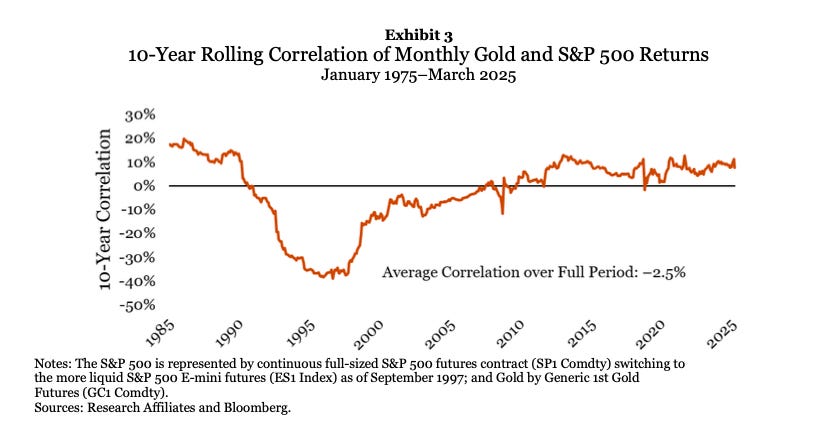

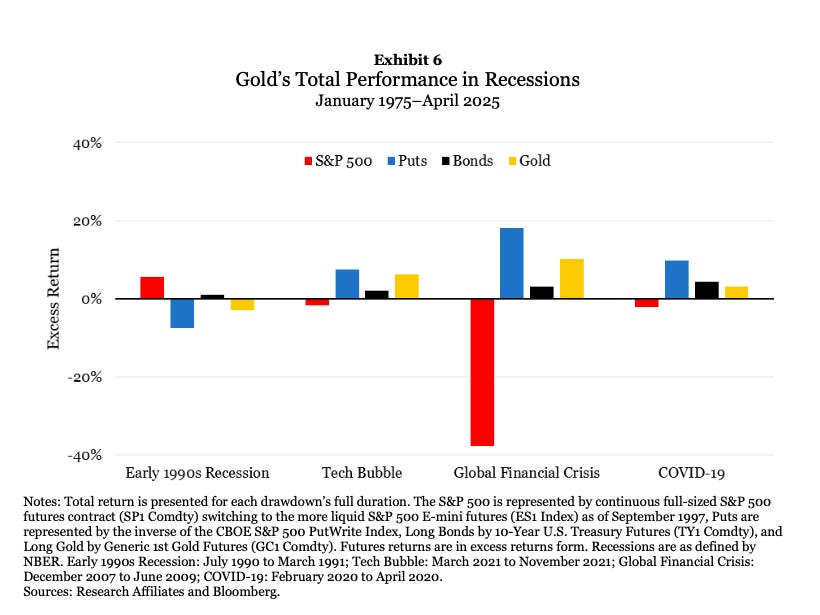

But here’s where it gets interesting. Add gold to a stock portfolio and something magical happens—your overall volatility drops. Gold and the S&P 500, an index of stocks, have basically zero correlation.1 They move independently. During the last 11 major stock market drawdowns, gold’s price actually rose in eight of them.

That’s the diversification benefit everyone talks about, as it reduces the risk of your overall portfolio. With stock market volatility feeling increasingly unpredictable, gold has proven it can be a genuine hedge. The correlation stays low and stable, which means when stocks are tanking, gold often isn’t.

But none of that explains why gold just hit all-time highs. For that, we need to look at what’s really driving demand.

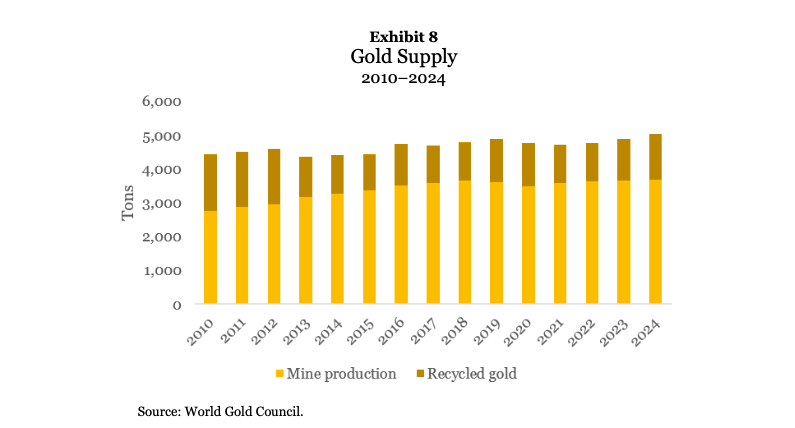

Gold supply is remarkably static. You can’t just make more gold—you have to mine it or recycle it. And mining gold is hard. That difficulty is actually why gold is so volatile in the first place. Supply can’t respond quickly to demand.

Demand, though? That’s a different story. In 2024, jewelry accounted for 44% of gold demand, investment for 26%, central banks and institutions for 23%, and technology for the remaining 7%.

Now here’s where human behavior gets fascinating. When gold prices rise, jewelry demand crashes. The correlation is strongly negative—about -0.64. Makes sense, right? Gold gets expensive, people buy fewer gold necklaces.

But investment demand? It does the opposite. ETF investors have a 0.71 positive correlation with gold prices. The more expensive gold gets, the more they buy. They’re price chasers, momentum investors, FOMO sufferers—pick your term. They see gold going up and pile in harder.

Central banks and institutions are more measured—they tend to buy less when prices rise. Tech demand barely responds to price at all.

So as jewelry demand collapses, ETF demand surges. And that’s creating something unprecedented.

Before November 18, 2004, if you wanted to invest in gold in the U.S., you had two options: buy physical gold (expensive, illiquid, with spreads of 5-8%) or buy gold mining stocks (which, spoiler alert, perform way worse than actual gold).

Then SPDR Gold Shares—ticker GLD—launched. The first gold-backed ETF. And suddenly, gold became completely financialized.

The growth was explosive because the demand had always been there—it was just suppressed by logistics. Institutional investors wanted gold exposure but couldn’t easily get it. Now they could buy it as easily as any stock.

And this is where economics gets broken. In a normal market, demand curves slope downward. Price goes up, demand goes down. But gold ETFs have an upward-sloping demand curve. Higher price, higher demand.

In economics, there are only two types of goods that do this: Giffen goods (staples like bread during famines) and Veblen goods (luxury status items like Birkin bags). Gold is neither. It’s not a staple. It’s not a status symbol in the way a Rolex is.

So what is it? Two things. First, momentum investing—people genuinely believe the price will keep rising. Second, it’s becoming a “security of last resort.” During stressful periods, when everything else feels risky, gold is where people run. And that hedging demand drives the price up further.

From 2004 to 2022, ETF flows and gold prices had a 0.92 correlation. Nearly perfect. But from 2023 to 2025? That correlation vanished. Went negative, actually.

Which means something else is driving gold prices now.

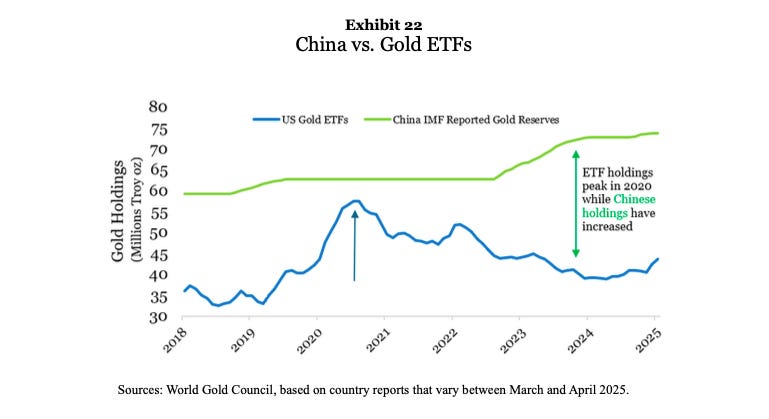

China is buying gold. A lot of gold. So is Russia. And it’s not because they think it’s a good investment.

China is actively working to reduce dependence on the U.S. dollar. Geopolitical tensions are rising. Trade wars, technology restrictions, military posturing—all of it makes dollar-denominated assets feel risky if you’re China.

Gold is the logical alternative. It’s neutral. No country controls it. You can’t sanction someone’s gold reserves the way you can freeze dollar assets.

China’s official gold reserves have spiked dramatically in recent years. This isn’t retail investors FOMOing into GLD. This is nation-states making strategic moves that signal they’re preparing for a world where the dollar isn’t the only game in town.

But what does all of this mean for you?

Here’s what the data says. Over the very long term, gold moves with inflation and delivers a real return of basically zero. It’s volatile in the short term, but over decades, it just keeps pace with the cost of living.

For that long-term average real return to be zero, periods of positive returns have to be offset by periods of negative returns. Gold’s real price mean reverts. Always has.

In 2012, researchers noticed gold’s real price was unusually high. They anticipated negative returns. And over the next five years, gold’s real price fell more than 12%.

Right now, based on historical patterns, gold is expensive again. Which suggests expected returns should be very low—possibly negative—over the next decade.

But here’s the thing your dad won’t tell you at Christmas: he didn’t buy gold to get rich. He bought it because when everything else is chaos, gold is still gold. It’s insurance, not investment. It’s the asset you hope you never need to cash in.

The world is fracturing in ways we haven’t seen in decades. Central banks are diversifying away from dollars. Geopolitical tensions are escalating. Traditional alliances are straining. In that context, gold isn’t about returns. It’s about having something that holds value no matter what happens.

So yes, your parents were right about gold. But maybe not for the reasons they think. And you weren’t entirely wrong about Bitcoin either—you were just early to a bigger conversation about what money even means when trust in institutions is eroding.

The real lesson? Sometimes the boring, traditional answer is right not because it’s exciting, but because it survives. Gold has outlasted every currency, every empire, every financial innovation. And in uncertain times, survival matters more than performance.

Pass the cranberry sauce.

Claude B. Erb and Campbell R. Harvey, Understanding Gold (Los Angeles, CA: Claude B. Erb; Durham, NC: Duke University; Cambridge, MA: National Bureau of Economic Research, 2013).